UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

|

Investment Company Act file number:

|

811-08025

|

Global Income Fund, Inc.

(Exact name of registrant as specified in charter)

| 11 Hanover Square, New York, NY |

10005 |

| (Address of principal executive offices) |

(Zipcode) |

John F. Ramírez, Esq.

11 Hanover Square

New York, NY 10005

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-212-344-6310

Date of fiscal year end: 12/31

Date of reporting period: 1/1/11 - 12/31/11

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a current valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under clearance requirements of 44 U.S.C. sec. 3507.

Item 1. Report to Shareholders.

COUNTRY ALLOCATION*

PORTFOLIO ANALYSIS*

|

Currency Allocation

|

|

Bond Ratings

|

|

U.S. Dollars**

|

79%

|

|

AAA

|

0%

|

|

Euros

|

5%

|

|

AA

|

4%

|

|

Australian Dollars

|

7%

|

|

A

|

8%

|

|

Canadian Dollars

|

2%

|

|

BBB

|

3%

|

| |

93%

|

|

<BBB

|

1%

|

| |

|

|

Non-bond investments***

|

77%

|

| |

|

|

|

93%

|

|

*

|

Country allocation and portfolio analysis use approximate percentages of net assets and may not add up to 100% due to leverage or other assets, rounding, and other factors. Ratings are not a guarantee of credit quality and may change. U.S. allocation may include closed end funds that may invest in foreign securities.

|

|

**

|

May include allocation to closed end funds that may invest in securities denominated in foreign currencies.

|

|

***

|

Non-bond investments include closed end funds that may invest in bonds, including non-investment grade “junk bonds” rated <BBB.

|

| |

|

GLOBAL INCOME

|

|

|

FUND

|

Ticker: GIFD

|

| |

|

|

11 Hanover Square, New York, NY 10005

|

|

|

|

www.GlobalIncomeFund.net

|

|

|

|

| |

|

|

February 3, 2012

|

Dear Fellow Shareholders:

It is a pleasure to submit this 2011 Annual Report for Global Income Fund and to welcome our new shareholders who find the Fund’s quality approach attractive. As a reminder, the primary and fundamental objective of the Fund is to provide a high level of income. The Fund’s secondary, non-fundamental investment objective is capital appreciation. The Fund currently pursues its investment objectives by investing primarily in closed end funds that invest significantly in income producing securities and a global portfolio of investment grade fixed income securities.

Investing in Real Estate Investment Trusts

In addition to closed end funds and fixed income securities, in seeking its investment objectives the Fund currently intends to begin to invest also in real estate investment trusts (“REITs”). A REIT is a corporation, business trust, or association that essentially combines the capital of many investors to acquire or provide financing for all forms of real estate. Distributions received by the Fund from REITs may be attributable to net investment income, net realized capital gains, and/or returns of capital. Like the registered closed end funds in which the Fund currently invests, a company that qualifies as a REIT generally is not subject to federal corporate income tax on its net income and net realized gains that it distributes to its shareholders, provided certain tax requirements are satisfied, although dividends paid by REITs will generally not qualify for the reduced federal income tax rates applicable to “qualified dividend income” under current tax rules. The market value of a REIT’s shares and its ability to distribute income may be affected by numerous factors, including: features of the REIT’s underlying properties and other assets, such as management, maintenance, safety, convenience, and attractiveness; competition for properties, tenants, personnel, and capital; interest rates; costs of compliance with zoning, environmental, disability, and other laws and local rules; real estate taxes, insurance, and other operating expenses; the national, state, and local economic climate and real estate conditions; governmental rules and policies; and other factors within and beyond the control of the REIT. Nevertheless, although there can be no assurances, the Fund believes that REIT investing may help the Fund achieve its investment objectives.

Global Economic and Market Report

In 2011, real gross domestic product (GDP), or the output of goods and services produced by labor and property located in the United States, increased only 1.6%, as compared to an increase of 3.1% in 2010, according to a recent report of the U.S. Bureau of Economic Analysis. In an announcement well received by financial markets, to support the moderately expanding economy, the Federal Open Market Committee (FOMC) has indicated that it would keep the target range for the federal funds interest rate at 0% to 0.25%. Offsetting this potential reason for optimism, the FOMC also indicated that it anticipates subdued economic conditions, including low rates of resource utilization, likely to warrant exceptionally low levels for the federal funds interest rate at least through late 2014. While the FOMC has noted that there appears to be some improvement in overall labor market conditions, the FOMC seems to view the unemployment rate as elevated and, although household spending has continued to advance, it observes that growth in business fixed investment has slowed and the housing sector remains depressed. Interestingly, inflation over the 2011 year as measured by the Consumer Price Index increased 3.0% before seasonal adjustment.

Globally, we are concerned by a further slowing of the Chinese economy and with the Eurozone's sovereign debt and banking industry issues. We note that China’s GDP was reported by the National Bureau of Statistics to have grown 9.2% in of 2011, impressive but slowing from previously higher levels, although inflation has apparently eased to a 4.1% annualized rate. European growth is subdued, expanding 1.4% in the third quarter of 2011 over the same quarter in the previous year, while unemployment continues to exceed 10%. Meanwhile, Japan’s economy has shown little progress in escaping its current quagmire, contracting three quarters in a row – most recently shrinking 0.7% in the third quarter of 2011 over the same quarter in 2010, while experiencing mild deflation and benchmark government interest rates at essentially zero.

Global Strategy for a High Level of Income

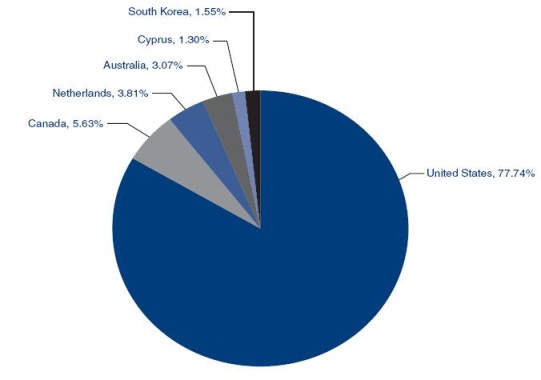

Given this slowing economic environment, the Fund’s strategy in 2011 included investing its assets primarily in closed end funds that invest significantly in income producing securities and a global portfolio of investment grade fixed income securities denominated in major world currencies and issued by organizations across many countries. At December 31, 2011, holdings of closed end funds and closed end fund business development companies comprised approximately 61% of the Fund’s investments. In its global portfolio of fixed income securities, the Fund held securities of governments, corporations, and other organizations based in Australia, Canada, Cyprus, Netherlands, South Korea, and the United States. In 2011, the Fund had a net asset value return per share of (1.86)% on a market price return per share for the period of (3.30)%, reflecting an increased market price discount to net asset value. Recently, the Fund’s net asset value per share was $4.89 and its share closing market price was $3.88. While investment return and value will vary and shares of the Fund may subsequently be worth more or less than their original cost, this represents an opportunity for investors to purchase the Fund’s shares at a discount to their underlying net asset value.

Fund Website and Dividend Reinvestment Plan

The Fund’s website, www.globalincomefund.net, provides investors with investment information, news, and other material regarding the Fund. You are invited to use this excellent resource to learn more about the Fund.

Thank you for investing in the Fund. As always, we are grateful to the Fund's long standing shareholders for their continuing support. For those shareholders currently receiving the Fund’s quarterly dividends in cash but are interested in adding to their account through the Fund’s Dividend Reinvestment Plan, we encourage you to review the Plan set forth later in this document and contact the Transfer Agent, who will be pleased to assist you with no obligation on your part.

| |

Sincerely, |

| |

|

| |

Thomas B. Winmill |

| |

President |

SCHEDULE OF PORTFOLIO INVESTMENTS - December 31, 2011

|

Shares

|

|

|

|

Cost

|

|

|

Value

|

|

| |

|

CLOSED END FUNDS (49.14%)

|

|

|

|

|

|

|

| |

|

United States

|

|

|

|

|

|

|

| |

135,000 |

|

AllianceBernstein Income Fund, Inc

|

|

$ |

1,061,384 |

|

|

$ |

1,089,450 |

|

| |

124,037 |

|

Alpine Global Premier Properties Fund

|

|

|

767,174 |

|

|

|

657,396 |

|

| |

100,000 |

|

BlackRock Credit Allocation Income Trust I, Inc

|

|

|

895,205 |

|

|

|

929,000 |

|

| |

110,000 |

|

BlackRock Credit Allocation Income Trust II, Inc

|

|

|

1,123,134 |

|

|

|

1,081,300 |

|

| |

90,000 |

|

BlackRock Credit Allocation Income Trust III, Inc

|

|

|

1,011,567 |

|

|

|

948,600 |

|

| |

104,900 |

|

BlackRock Income Trust, Inc

|

|

|

609,177 |

|

|

|

768,917 |

|

| |

125,425 |

|

Calamos Strategic Total Return Fund

|

|

|

1,089,887 |

|

|

|

1,047,299 |

|

| |

78,288 |

|

Clough Global Allocation Fund

|

|

|

1,207,710 |

|

|

|

998,172 |

|

| |

77,579 |

|

Cohen & Steers Infrastructure Fund, Inc

|

|

|

1,064,457 |

|

|

|

1,228,076 |

|

| |

65,675 |

|

First Trust Strategic High Income Fund II

|

|

|

880,888 |

|

|

|

1,003,514 |

|

| |

54,000 |

|

Gabelli Dividend & Income Trust

|

|

|

827,901 |

|

|

|

832,680 |

|

| |

15,800 |

|

Helios Advantage Income Fund, Inc

|

|

|

123,824 |

|

|

|

123,556 |

|

| |

69,329 |

|

Lazard World Dividend & Income Fund, Inc

|

|

|

792,432 |

|

|

|

750,833 |

|

| |

48,151 |

|

Macquarie/First Trust Global Infrastructure/Utilities Dividend

|

|

|

|

|

|

|

|

|

| |

|

|

& Income Fund

|

|

|

593,377 |

|

|

|

684,226 |

|

| |

66,054 |

|

Macquarie Global Infrastructure Total Return Fund Inc

|

|

|

1,077,799 |

|

|

|

1,122,257 |

|

| |

62,000 |

|

Nuveen Diversified Dividend and Income Fund

|

|

|

618,254 |

|

|

|

636,120 |

|

| |

93,000 |

|

Nuveen Multi-Strategy Income & Growth Fund 2

|

|

|

812,547 |

|

|

|

748,650 |

|

| |

20,000 |

|

Source Capital, Inc

|

|

|

1,088,630 |

|

|

|

939,600 |

|

| |

64,845 |

|

Western Asset Global Corporate Defined Opportunity Fund Inc

|

|

|

1,159,565 |

|

|

|

1,167,211 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

Total closed end funds

|

|

|

16,804,912 |

|

|

|

16,756,857 |

|

|

Principal

|

|

|

|

|

|

|

|

|

|

Account(a)

|

|

|

|

|

|

|

|

|

| |

|

DEBT SECURITIES (15.67%)

|

|

|

|

|

|

|

| |

|

Australia (3.07%)

|

|

|

|

|

|

|

| |

$A500,000 |

|

Telstra Corp. Ltd., 6.25% Senior Notes, due 4/15/15

|

|

|

365,869 |

|

|

|

524,193 |

|

| |

$A500,000 |

|

Telstra Corp. Ltd., 7.25% Senior Notes, due 11/15/12

|

|

|

369,404 |

|

|

|

522,893 |

|

| |

|

|

|

|

|

735,273 |

|

|

|

1,047,086 |

|

| |

|

|

Canada (5.63%)

|

|

|

|

|

|

|

|

|

| |

$C500,000 |

|

Molson Coors Capital Finance, 5.00% Guaranteed Notes,

|

|

|

|

|

|

|

|

|

| |

|

|

due 9/22/15

|

|

|

448,784 |

|

|

|

528,691 |

|

| |

$A1,350,000 |

|

Province of Ontario, 5.50% Euro Medium Term Notes, due 7/13/12

|

|

|

1,043,008 |

|

|

|

1,390,401 |

|

| |

|

|

|

|

|

1,491,792 |

|

|

|

1,919,092 |

|

| |

|

|

Cyprus (1.30%)

|

|

|

|

|

|

|

|

|

| |

€500,000 |

|

Republic of Cyprus, 4.375% Euro Medium Term Notes, due 7/15/14

|

|

|

619,472 |

|

|

|

441,877 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

Netherlands (3.81%)

|

|

|

|

|

|

|

|

|

| |

€1,000,000 |

|

ING Bank N.V., 5.50% Euro Medium Term Notes, due 1/04/12

|

|

|

1,282,440 |

|

|

|

1,298,145 |

|

SCHEDULE OF PORTFOLIO INVESTMENTS (CONCLUDED)

|

Principal

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

DEBT SECURITIES (continued)

|

|

|

|

|

|

|

| |

|

South Korea (1.55%)

|

|

|

|

|

|

|

| |

500,000 |

|

Korea Development Bank, 5.75% Notes, due 9/10/13

|

|

$ |

503,212 |

|

|

$ |

529,095 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

United States (0.31%)

|

|

|

|

|

|

|

|

|

| |

135,229 |

|

CIT RV Trust 1998-A B 6.29% Subordinated Bonds, due 1/15/17

|

|

|

136,993 |

|

|

|

107,336 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

Total debt securities

|

|

|

4,769,182 |

|

|

|

5,342,631 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

CLOSED END FUND BUSINESS DEVELOPMENT

|

|

|

|

|

|

|

|

|

|

|

|

COMPANIES (11.73%)

|

|

|

|

|

|

|

|

|

| |

|

|

United States

|

|

|

|

|

|

|

|

|

| |

116,000 |

|

American Capital, Ltd

|

|

|

1,146,277 |

|

|

|

780,680 |

|

| |

12,500 |

|

Capital Southwest Corp

|

|

|

1,165,713 |

|

|

|

1,019,375 |

|

| |

110,000 |

|

MCG Capital Corp

|

|

|

662,176 |

|

|

|

438,900 |

|

| |

140,845 |

|

NGP Capital Resources Co

|

|

|

1,015,388 |

|

|

|

1,012,676 |

|

| |

60,598 |

|

Saratoga Investment Corp

|

|

|

1,270,962 |

|

|

|

748,385 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

Total closed end fund business development companies

|

|

|

5,260,516 |

|

|

|

4,000,016 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

PREFERRED STOCKS (1.59%)

|

|

|

|

|

|

|

|

|

| |

|

|

United States

|

|

|

|

|

|

|

|

|

| |

4,000 |

|

BAC Capital Trust II, 7.00%

|

|

|

100,000 |

|

|

|

83,560 |

|

| |

17,834 |

|

Corporate-Backed Trust Certificates, 8.20% (Motorola)

|

|

|

445,850 |

|

|

|

459,939 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

Total preferred stocks

|

|

|

545,850 |

|

|

|

543,499 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

MONEY MARKET FUND (14.97%)

|

|

|

|

|

|

|

|

|

| |

|

|

United States

|

|

|

|

|

|

|

|

|

| |

5,106,774 |

|

SSgA Money Market Fund, 7 day annualized yield 0.01%

|

|

|

5,106,774 |

|

|

|

5,106,774 |

|

| |

|

|

Total investments (93.10%)

|

|

$ |

32,487,234 |

|

|

|

31,749,777 |

|

| |

|

|

Other assets in excess of liabilities (6.90%)

|

|

|

|

|

|

|

2,351,804 |

|

| |

|

|

Net assets (100.00%)

|

|

|

|

|

|

$ |

34,101,581 |

|

|

(a)

|

The principal amount is stated in U.S. dollars unless otherwise indicated.

|

| |

Currency Symbols |

| |

A$ Australian Dollar |

| |

C$ Canadian Dollar |

| |

€ Euro |

See notes to financial statements.

|

STATEMENT OF ASSETS AND LIABILITIES

|

|

|

December 31, 2011

|

|

|

|

| |

|

|

|

|

ASSETS

|

|

|

|

|

Investments, at value (cost: $32,487,234)

|

|

$ |

31,749,777 |

|

|

Receivables

|

|

|

1,958,988 |

|

|

Securities sold

|

|

|

|

|

|

Dividends

|

|

|

353,881 |

|

|

Interest

|

|

|

147,452 |

|

|

Other assets

|

|

|

14,993 |

|

|

Total assets

|

|

|

34,225,091 |

|

| |

|

|

|

|

|

LIABILITIES

|

|

|

|

|

|

Payables

|

|

|

|

|

|

Accrued expenses

|

|

|

94,797 |

|

|

Investment management

|

|

|

20,204 |

|

|

Administrative services

|

|

|

8,509 |

|

|

Total liabilities

|

|

|

123,510 |

|

| |

|

|

|

|

|

NET ASSETS

|

|

$ |

34,101,581 |

|

| |

|

|

|

|

|

NET ASSET VALUE PER SHARE

|

|

|

|

|

|

(applicable to 7,415,983 shares

|

|

|

|

|

|

outstanding: 20,000,000 shares of $.01

|

|

|

|

|

|

par value authorized)

|

|

$ |

4.60 |

|

| |

|

|

|

|

|

NET ASSETS CONSIST OF

|

|

|

|

|

|

Paid in capital

|

|

$ |

33,239,454 |

|

|

Accumulated net investment loss

|

|

|

(864 |

) |

|

Accumulated net realized gain on

|

|

|

|

|

|

investments and foreign currencies

|

|

|

1,606,376 |

|

|

Net unrealized depreciation on

|

|

|

|

|

|

investments and foreign currencies

|

|

|

(743,385 |

) |

| |

|

$ |

34,101,581 |

|

|

STATEMENT OF OPERATIONS

|

|

|

|

|

Year Ended December 31, 2011

|

|

|

|

| |

|

|

|

|

INVESTMENT INCOME

|

|

|

|

|

Dividends

|

|

$ |

1,906,714 |

|

|

Interest

|

|

|

332,776 |

|

|

Total investment income

|

|

|

2,239,490 |

|

| |

|

|

|

|

|

EXPENSES

|

|

|

|

|

|

Legal

|

|

|

369,414 |

|

|

Investment management

|

|

|

257,203 |

|

|

Directors

|

|

|

56,639 |

|

|

Administrative services

|

|

|

44,185 |

|

|

Bookkeeping and pricing

|

|

|

38,960 |

|

|

Shareholder communications

|

|

|

27,759 |

|

|

Auditing

|

|

|

23,595 |

|

|

Insurance

|

|

|

9,310 |

|

|

Transfer agent

|

|

|

6,820 |

|

|

Custodian

|

|

|

6,590 |

|

|

Interest and fees on bank credit facility

|

|

|

3,417 |

|

|

Other

|

|

|

3,325 |

|

|

Total expenses

|

|

|

847,217 |

|

|

Net investment income

|

|

|

1,392,273 |

|

| |

|

|

|

|

|

REALIZED AND UNREALIZED GAIN (LOSS)

|

|

|

|

|

|

Net realized gain (loss)

|

|

|

|

|

|

Investments

|

|

|

3,672,403 |

|

|

Foreign currencies

|

|

|

(20,110 |

) |

|

Net unrealized depreciation

|

|

|

|

|

|

Investments

|

|

|

(6,084,531 |

) |

|

Translation of assets and liabilities

|

|

|

|

|

| in foreign currencies |

|

|

(17,619 |

) |

|

Net realized and unrealized loss

|

|

|

(2,449,857 |

) |

|

Net decrease in net assets

|

|

|

|

|

|

resulting from operations

|

|

$ |

(1,057,584 |

) |

See notes to financial statements.

| STATEMENTS OF CHANGES IN NET ASSETS |

|

|

|

|

|

|

| For the Years Ended December 31, 2011 and 2010 |

|

|

|

|

|

|

| |

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

OPERATIONS

|

|

|

|

|

|

|

|

Net investment income

|

|

$ |

1,392,273 |

|

|

$ |

1,470,996 |

|

|

Net realized gain

|

|

|

3,652,293 |

|

|

|

2,459,454 |

|

|

Unrealized appreciation (depreciation)

|

|

|

(6,102,150 |

) |

|

|

1,945,253 |

|

| |

|

|

|

|

|

|

|

|

|

Net increase (decrease) in net assets resulting from operations

|

|

|

(1,057,584 |

) |

|

|

5,875,703 |

|

| |

|

|

|

|

|

|

|

|

|

DISTRIBUTIONS TO SHAREHOLDERS

|

|

|

|

|

|

|

|

|

|

Distributions from ordinary income ($0.26 and $0.22 per share, respectively)

|

|

|

(1,927,516 |

) |

|

|

(1,630,219 |

) |

| |

|

|

|

|

|

|

|

|

|

CAPITAL SHARE TRANSACTIONS

|

|

|

|

|

|

|

|

|

|

Reinvestment of distributions to shareholders (3,888 and 3,212 shares, respectively)

|

|

|

15,562 |

|

|

|

12,144 |

|

| |

|

|

|

|

|

|

|

|

|

Total change in net assets

|

|

|

(2,969,538 |

) |

|

|

4,257,628 |

|

| |

|

|

|

|

|

|

|

|

|

NET ASSETS

|

|

|

|

|

|

|

|

|

|

Beginning of period

|

|

|

37,071,119 |

|

|

|

32,813,491 |

|

| |

|

|

|

|

|

|

|

|

|

End of period

|

|

$ |

34,101,581 |

|

|

$ |

37,071,119 |

|

| |

|

|

|

|

|

|

|

|

|

End of period net assets include undistributed net investment income (loss)

|

|

$ |

(864 |

) |

|

$ |

129,680 |

|

See notes to financial statements.

NOTES TO FINANCIAL STATEMENTS – DECEMBER 31, 2011

1. Organization and Significant Accounting Policies

Global Income Fund, Inc., a Maryland corporation registered under the Investment Company Act of 1940, as amended (the “Act”), is a non-diversified, closed end management investment company, whose shares are quoted over the counter under the ticker symbol GIFD. The Fund’s investment objectives are primarily to provide a high level of income and, secondarily, capital appreciation. The Fund retains CEF Advisers, Inc. as its Investment Manager.

The following is a summary of the Fund’s significant accounting policies:

Valuation of Investments – Portfolio securities are valued by various methods depending on the primary market or exchange on which they trade. Most equity securities for which the primary market is in the United States are valued at the official closing price, last sale price or, if no sale has occurred, at the closing bid price. Most equity securities for which the primary market is outside the United States are valued using the official closing price or the last sale price in the principal market in which they are traded. If the last sale price on the local exchange is unavailable, the last evaluated quote or closing bid price normally is used. Debt obligations with remaining maturities of 60 days or less are valued at cost adjusted for amortization of premiums and accretion of discounts. Certain of the securities in which the Fund may invest are priced through pricing services that may utilize a matrix pricing system which takes into consideration factors such as yields, prices, maturities, call features, and ratings on comparable securities. Bonds may be valued according to prices quoted by a bond dealer that offers pricing services. Open end investment companies are valued at their net asset value. Foreign securities markets may be open on days when the U.S. markets are closed. For this reason, the value of any foreign securities owned by the Fund could change on a day when stockholders cannot buy or sell shares of the Fund. Securities for which market quotations are not readily available or reliable and other assets may be valued as determined in good faith by the Investment Manager under the direction of or pursuant to procedures established or approved by the Fund’s Board of Directors, called “fair value pricing.” Due to the inherent uncertainty of valuation, fair value pricing values may differ from the values that would have been used had a readily available market for the securities existed. These differences in valuation could be material. A security’s valuation may differ depending on the method used for determining value. The use of fair value pricing by the Fund may cause the net asset value of its shares to differ from the net asset value that would be calculated using market prices.

Foreign Currency Translation – Securities denominated in foreign currencies are translated into U.S. dollars at prevailing exchange rates. Realized gain or loss on sales of such investments in local currency terms is reported separately from gain or loss attributable to a change in foreign exchange rates for those investments.

Foreign Currency Contracts – Forward foreign currency contracts are marked to market and the change in market value is recorded by the Fund as an unrealized gain or loss. When a contract is closed, the Fund records a realized gain or loss equal to the difference between the value of the contract at the time it was opened and the value at the time it was closed. The Fund could be exposed to risk if the counterparties are unable to meet the terms of the contracts or if the value of the currency changes unfavorably.

Investments in Other Investment Companies – The Fund may invest in shares of other investment companies (the “Acquired Funds”) in accordance with the Act and related rules. Shareholders in the Fund bear the pro rata portion of the fees and expenses of the Acquired Funds in addition to the Fund’s expenses. Expenses incurred by the Fund that are disclosed in the Statement of Operations do not include fees and expenses incurred by the Acquired Funds. The fees and expenses of the Acquired Funds are reflected in the Fund’s total returns.

Short Sales – The Fund may sell a security short it does not own in anticipation of a decline in the market value of the security. When the Fund sells a security short, it must borrow the security sold short and deliver it to the broker/dealer through which it made the short sale. The Fund is liable for any dividends or interest paid on securities sold short. A gain, limited to the price at which the Fund sold the security short, or a loss, unlimited in size, will be recognized upon the termination of the short sale. Securities sold short result in off balance sheet risk as the Fund’s ultimate obligation to satisfy the terms of the sale of securities sold short may exceed the amount recognized in the Statement of Assets and Liabilities.

NOTES TO FINANCIAL STATEMENTS (Continued)

Investment Transactions – Investment transactions are accounted for on the trade date (the date the order to buy or sell is executed). Realized gains or losses are determined by specifically identifying the cost basis of the investment sold.

Investment Income – Interest income is recorded on the accrual basis. Amortization of premium and accretion of discount on debt securities are included in interest income. Dividend income is recorded on the ex-dividend date or, in the case of foreign securities, as soon as the Fund is notified. Taxes withheld on income from foreign securities have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates.

Expenses – Expenses deemed by the Investment Manager to have been incurred solely by the Fund are charged to the Fund. Expenses deemed by the Investment Manager to have been incurred jointly by the Fund and one or more of the other investment companies for which the Investment Manager or its affiliates serve as investment manager (the “Fund Complex”) or other entities are allocated on the basis of relative net assets, except where a more appropriate allocation can be made fairly in the judgment of the Investment Manager.

Expense Reduction Arrangement – Through arrangements with the Fund’s custodian and cash management bank, credits realized as a result of uninvested cash balances are used to reduce custodian expenses. No credits were realized by the Fund during the periods covered by this report.

Distributions to Shareholders – Distributions to shareholders, are determined in accordance with income tax regulations and are recorded on the ex-dividend date.

Income Taxes – No provision has been made for U.S. income taxes because the Fund’s current intention is to continue to qualify as a regulated investment company under the Internal Revenue Code (the “IRC”) and to distribute to its shareholders substantially all of its taxable income and net realized gains. Foreign securities held by the Fund may be subject to foreign taxation. Foreign taxes, if any, are recorded based on the tax regulations and rates that exist in the foreign markets in which the Fund invests. The Fund recognizes the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. The Fund has reviewed its tax positions and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on federal, state, and local income tax returns for open tax years (2008 – 2010), or expected to be taken in the Fund’s 2011 tax returns.

Use of Estimates – In preparing financial statements in conformity with accounting principles generally accepted in the United States of America (“GAAP”), management makes estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements, as well as the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Recent Accounting Standards Update – In May 2011, the Financial Accounting Standards Board issued Accounting Standards Update (“ASU”) 2011-04 “Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs (“International Financial Reporting Standards”).” ASU 2011-04 includes common requirements for measurement of and disclosure about fair value between GAAP and IFRS. ASU 2011-04 will require disclosure of the following information for fair value measurements categorized within level 3 of the fair value hierarchy: quantitative information about the unobservable inputs used in the fair value measurement, the valuation processes used by the Fund, and a narrative description of the sensitivity of the fair value measurement to changes in unobservable inputs and the interrelationships between those unobservable inputs. In addition, ASU 2011-04 will require disclosures about amounts and reasons for all transfers in and out of level 1 and level 2 fair value measurements. ASU 2011-04 is effective for interim and annual reporting periods beginning after December 15, 2011. The Fund has concluded that upon adoption of ASU 2011-04 the Fund’s financial statements and accompanying notes will fully comply with the required new and revised disclosures.

In December 2011, FASB issued ASU 2011-11 “Disclosures about Offsetting Assets and Liabilities.” The amendments in ASU 2011-11 will require the Fund to disclose information about offsetting and related arrangements to enable users of its financial statements to understand the effect of those arrangements on its financial position. ASU 2011-11 is effective for annual reporting periods beginning on or after January 1, 2013, and interim periods within those annual periods. ASU 2011-11 requires retrospective application for all comparative periods presented. The Fund is evaluating ASU 2011-11 and the impact it may have to its financial statement disclosures.

NOTES TO FINANCIAL STATEMENTS (Continued)

2. Fees and Transactions with Related Parties

The Fund retains the Investment Manager pursuant to an Investment Management Agreement (“IMA”). Under the terms of the IMA, the Investment Manager receives a management fee, payable monthly, based on the average daily net assets of the Fund at an annual rate of 7/10 of 1% of the first $50 million, 5/8 of 1% over $50 million to $150 million, and 1/2 of 1% over $150 million. Certain officers and directors of the Fund are officers and directors of the Investment Manager. Pursuant to the IMA, the Fund reimburses the Investment Manager for providing at cost certain administrative services comprised of compliance and accounting services. For the year ended December 31, 2011, the Fund incurred total administrative costs of $44,185, comprised of $33,420 and $10,765 for compliance and accounting services, respectively.

3. Distributions to Shareholders and Distributable Earnings

The tax character of distributions paid to shareholders was as follows:

| |

|

Year Ended

|

|

|

Year Ended

|

|

| |

|

|

|

|

|

|

|

Ordinary income

|

|

$ |

1,927,516 |

|

|

$ |

1,630,219 |

|

| |

|

|

The components of distributable earnings on a tax basis were as follows:

|

|

| |

|

|

|

|

|

|

|

|

|

Undistributed net capital gains

|

|

|

|

|

|

$ |

1,606,376 |

|

|

Unrealized depreciation on investments and foreign currencies

|

|

|

|

|

|

|

(743,385) |

|

|

Post-October currency losses

|

|

|

|

|

|

|

(864) |

|

| |

|

|

|

|

|

$ |

862,127 |

|

Federal income tax regulations permit post-October net capital and currency losses, if any, to be deferred and recognized on the tax return of the next succeeding taxable year.

GAAP requires certain components of net assets to be classified differently for financial reporting than for tax reporting purposes. While these differences have no effect on net assets or net asset value per share, these differences may result in distribution reclassifications. Primarily due to differences in treatment of foreign currency transactions, and return of capital dividends, on December 31, 2011 the Fund recorded the following financial reporting adjustments to the identified accounts to reflect those differences:

| |

|

Decrease in

|

|

|

Increase in

|

Decrease in

|

Unrealized Depreciation

|

|

|

Undistributed

|

Net Realized Gain on

|

on Investments and

|

Decrease in

|

|

|

Investments and Foreign Currencies

|

|

|

|

$404,698

|

$(498,278)

|

$141,084

|

$(47,504)

|

4. Fair Value Measurements

GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of inputs are:

• Level 1 – unadjusted quoted prices in active markets for identical assets or liabilities including securities actively traded on a securities exchange.

NOTES TO FINANCIAL STATEMENTS (Continued)

• Level 2 – observable inputs other than quoted prices included in level 1 that are observable for the asset or liability which may include quoted prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates, and similar data.

• Level 3 – unobservable inputs for the asset or liability including the Fund’s own assumptions a market participant would use in valuing the asset or liability.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for investments categorized in level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing investments are not an indication of the risk associated with investing in those securities.

The following is a description of the valuation techniques applied to the Fund’s major categories of assets and liabilities measured at fair value on a recurring basis:

Equity securities (common and preferred stock). Equity securities traded on a national securities exchange or market are stated normally at the official closing price, last sale price or, if no sale has occurred, at the closing bid price on the day of valuation. To the extent these securities are actively traded and valuation adjustments are not applied, they may be categorized in level 1 of the fair value hierarchy. Preferred stock and other equities on inactive markets or valued by reference to similar instruments may be categorized in level 2.

Debt securities. The fair value of debt securities is estimated using various techniques, which may consider, among other things, recently executed transactions in securities of the issuer or comparable issuers, market price quotations (where observable), bond spreads, and fundamental data relating to the issuer. Although most debt securities may be categorized in level 2 of the fair value hierarchy, in instances where lower relative consideration is placed on transaction prices, quotations, or similar observable inputs, they may be categorized in level 3.

The following is a summary of the inputs used as of December 31, 2011 in valuing the Fund’s assets carried at fair value. Refer to the Schedule of Portfolio Investments for detailed information on specific investments.

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Assets

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investments, at value

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Closed end funds

|

|

|

|

|

|

|

|

|

|

|

|

|

|

United States

|

|

$ |

16,756,857 |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

16,756,857 |

|

|

Debt securities

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Australia

|

|

|

— |

|

|

|

1,047,086 |

|

|

|

— |

|

|

|

1,047,086 |

|

|

Canada

|

|

|

— |

|

|

|

1,919,092 |

|

|

|

— |

|

|

|

1,919,092 |

|

|

Cyprus

|

|

|

— |

|

|

|

441,877 |

|

|

|

— |

|

|

|

441,877 |

|

|

Netherlands

|

|

|

— |

|

|

|

1,298,145 |

|

|

|

— |

|

|

|

1,298,145 |

|

|

South Korea

|

|

|

— |

|

|

|

529,095 |

|

|

|

— |

|

|

|

529,095 |

|

|

United States

|

|

|

— |

|

|

|

107,336 |

|

|

|

— |

|

|

|

107,336 |

|

NOTES TO FINANCIAL STATEMENTS (Continued)

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

Closed end fund business development companies

|

|

|

|

|

|

|

|

|

|

|

|

|

|

United States

|

|

|

4,000,016 |

|

|

|

— |

|

|

|

— |

|

|

|

4,000,016 |

|

|

Preferred stocks

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

United States

|

|

|

543,499 |

|

|

|

— |

|

|

|

— |

|

|

|

543,499 |

|

|

Money market fund

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

United States

|

|

|

5,106,774 |

|

|

|

— |

|

|

|

— |

|

|

|

5,106,774 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total investments, at value

|

|

$ |

26,407,146 |

|

|

$ |

5,342,631 |

|

|

$ |

— |

|

|

$ |

31,749,777 |

|

There were no transfers between level 1 and level 2 during the year ended December 31, 2011.

5. Investment Transactions

Purchases and proceeds or maturities of investment securities, excluding short term investments, were $7,916,446 and $15,768,537, respectively, for the year ended December 31, 2011. As of December 31, 2011, for federal income tax purposes the aggregate cost of investment securities was $32,487,234 and net unrealized depreciation was $737,457, comprised of gross unrealized appreciation of $1,468,234 and gross unrealized depreciation of $2,205,691.

6. Bank Credit Facility

Effective April 1, 2011, the Fund and certain other funds in the Fund Complex (the “Borrowers”) entered into a committed secured line of credit facility, which is subject to annual renewal, with State Street Bank and Trust Company (“SSB”), the Fund’s custodian. The aggregate amount of the credit facility is $30,000,000. The borrowing of each Borrower is collateralized by the underlying investments of such Borrower. SSB will make revolving loans to a Borrower not to exceed in the aggregate outstanding at any time with respect to any one Borrower the least of 30% of the total net assets (as defined in the line of credit facility) of a Borrower, the maximum amount permitted pursuant to each Borrower’s investment policies, or as permitted under the Act. The commitment fee on this facility is 0.15% per annum. All loans under this facility will be available at the Borrower’s option of (i) overnight Federal funds or (ii) LIBOR (30, 60, 90 days), each as in effect from time to time, plus 1.10% per annum. Prior to April 1, 2011, the aggregate amount of the credit facility was $10,000,000 and the loans under this facility were available at the Borrower’s option of (i) overnight Federal funds or (ii) LIBOR (30, 60, 90 days) plus 1.50% per annum. At December 31, 2011, there were no outstanding borrowings under the credit facility. For the year ended December 31, 2011, the Fund’s weighted average interest rate under the credit facility was 1.73% based on its balances outstanding during the period and the Fund’s average daily amount outstanding during the period was $14,102.

7. Foreign Securities Risk

Investments in the securities of foreign issuers involve special risks, including changes in foreign exchange rates and the possibility of future adverse political and economic developments, which could adversely affect the value of such securities. Moreover, securities in foreign issuers and markets may be less liquid and their prices more volatile than those of U.S. issuers and markets.

8. Capital Stock

The Fund is authorized to issue 20,000,000 shares of $0.01 par value common stock. Transactions in common stock consisting of shares issued in reinvestment of distributions for the years ended December 31, 2011 and 2010 were as follows:

| |

|

|

|

|

|

|

|

Shares issued

|

|

|

3,888 |

|

|

|

3,212 |

|

|

Increase in paid in capital

|

|

$ |

15,562 |

|

|

$ |

12,144 |

|

9. Share Repurchase Program

In accordance with Section 23(c) of the Act, the Fund may from time to time repurchase its shares in the open market at the discretion of and upon such terms as the Board of Directors shall determine. During the years ended December 31, 2011 and 2010, the Fund did not repurchase any of its shares.

10. Contingencies

The Fund indemnifies its officers and directors from certain liabilities that might arise from their performance of their duties for the Fund. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties and which may provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown as it involves future claims that may be made against the Fund under circumstances that have not occurred.

11. Other Information

The Fund may at times raise cash for investment by issuing shares through one or more offerings, including rights offerings. Proceeds from any such offerings will be invested in accordance with the investment objectives and policies of the Fund.

12. Business Proposal

The Fund has scheduled a Special Meeting of Shareholders, adjourned to February 29, 2012, in connection with a proposal to fundamentally change its business from a registered investment company investing primarily in closed end funds that invest significantly in income producing securities and a global portfolio of investment grade fixed income securities to an operating company that will own, operate, manage, acquire, develop and redevelop professionally managed self storage facilities and will seek to qualify as a real estate investment trust (“REIT”) for federal tax purposes (“Business Proposal”). Proxy materials for the Special Meeting, providing a detailed description of the Business Proposal, may be obtained at www.globalincomefund.net/proxy-statement.html.

13. Subsequent Events

The Fund has evaluated subsequent events through the date the financial statements were issued and determined that no subsequent events have occurred that require additional disclosure in the financial statements.

FINANCIAL HIGHLIGHTS

| |

|

|

|

| |

|

2011

|

|

|

2010

|

|

|

2009

|

|

|

2008

|

|

|

2007

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Per Share Operating Performance

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(for a share outstanding throughout each period)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net asset value, beginning of period

|

|

$ |

5.00 |

|

|

$ |

4.43 |

|

|

$ |

3.64 |

|

|

$ |

4.60 |

|

|

$ |

4.38 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income from investment operations:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net investment income(1)

|

|

|

.19 |

|

|

|

.20 |

|

|

|

.21 |

|

|

|

.19 |

|

|

|

.13 |

|

|

Net realized and unrealized gain (loss)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

on investments

|

|

|

(.33 |

) |

|

|

.59 |

|

|

|

.82 |

|

|

|

(.91 |

) |

|

|

.31 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total income from investment operations

|

|

|

(.14 |

) |

|

|

.79 |

|

|

|

1.03 |

|

|

|

(.72 |

) |

|

|

.44 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Less distributions:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net investment income

|

|

|

(.26 |

) |

|

|

(.22 |

) |

|

|

(.24 |

) |

|

|

(.24 |

) |

|

|

(.17 |

) |

|

Return of capital

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

– |

|

|

|

(.05 |

) |

|

Total distributions

|

|

|

(.26 |

) |

|

|

(.22 |

) |

|

|

(.24 |

) |

|

|

(.24 |

) |

|

|

(.22 |

) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net asset value, end of period

|

|

$ |

4.60 |

|

|

$ |

5.00 |

|

|

$ |

4.43 |

|

|

$ |

3.64 |

|

|

$ |

4.60 |

|

|

Market value, end of period

|

|

$ |

3.78 |

|

|

$ |

4.17 |

|

|

$ |

3.65 |

|

|

$ |

2.70 |

|

|

$ |

3.90 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Return (2)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Based on net asset value

|

|

|

(1.86 |

)% |

|

|

19.60 |

% |

|

|

31.03 |

% |

|

|

(14.94 |

)% |

|

|

11.00 |

% |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Based on market price

|

|

|

(3.30 |

)% |

|

|

21.07 |

% |

|

|

45.55 |

% |

|

|

(25.58 |

)% |

|

|

(1.39 |

)% |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ratios/Supplemental Data (3)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net assets, end of period (000’s omitted)

|

|

$ |

34,102 |

|

|

$ |

37,071 |

|

|

$ |

32,813 |

|

|

$ |

26,979 |

|

|

$ |

34,057 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ratio of total expenses to average net assets

|

|

|

2.31 |

% |

|

|

2.00 |

% |

|

|

1.62 |

% |

|

|

1.68 |

% |

|

|

1.77 |

% |

|

Ratio of net expenses to average net assets

|

|

|

2.31 |

% |

|

|

2.00 |

% |

|

|

1.62 |

% |

|

|

1.68 |

% |

|

|

1.77 |

% |

|

Ratio of net expenses excluding loan

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

interest and fees to average net assets

|

|

|

2.30 |

% |

|

|

1.96 |

% |

|

|

1.56 |

% |

|

|

1.66 |

% |

|

|

1.75 |

% |

|

Ratio of net investment income to

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

average net assets

|

|

|

4.31 |

% |

|

|

4.33 |

% |

|

|

5.23 |

% |

|

|

4.31 |

% |

|

|

2.91 |

% |

|

Portfolio turnover rate

|

|

|

22 |

% |

|

|

55 |

% |

|

|

48 |

% |

|

|

21 |

% |

|

|

10 |

% |

|

(1)

|

The per share amounts were calculated using the average number of common shares outstanding during the period.

|

|

(2)

|

Total return on a market value basis is calculated assuming a purchase of common stock on the opening of the first day and a sale on the clos- ing of the last day of each period reported. Dividends and distributions, if any, are assumed for purposes of this calculation to be reinvested at prices obtained under the Fund’s Dividend Reinvestment Plan. Generally, total return on a net asset value basis will be higher than total return on a market value basis in periods where there is an increase in the discount or a decrease in the premium of the market value to the net asset value from the beginning to the end of such periods. Conversely, total return on a net asset value basis will be lower than total return on a mar- ket value basis in periods where there is a decrease in the discount or an increase in the premium of the market value to the net asset value from the beginning to the end of such periods. Total return calculated for a period of less than one year is not annualized. The calculation does not reflect brokerage commissions, if any.

|

|

(3)

|

Expense and income ratios for 2008, 2009, 2010, and 2011 do not include expenses incurred by the Acquired Funds in which the Fund invests.

|

See notes to financial statements.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Shareholders of Global Income Fund, Inc.

We have audited the accompanying statement of assets and liabilities of Global Income Fund, Inc., including the schedule of portfolio investments as of December 31, 2011 and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years indicated thereon. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with auditing standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2011 by correspondence with the custodian. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Global Income Fund, Inc. as of December 31, 2011, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and the financial highlights for each of the five years indicated thereon, in conformity with accounting principles generally accepted in the United States of America.

TAIT, WELLER & BAKER LLP

Philadelphia, Pennsylvania

February 24, 2012

DIVIDEND REINVESTMENT PLAN

Terms and Conditions of the

2012 Amended Dividend Reinvestment Plan

1. Each shareholder (the “Shareholder”) holding shares of common stock (the “Shares”) of Global Income Fund, Inc. (the “Fund”) will automatically be a participant in the Dividend Reinvestment Plan (the “Plan”), unless the Shareholder specifically elects to receive all dividends and capital gains in cash paid by check mailed directly to the Shareholder by American Stock Transfer & Trust Company, LLC, 6201 15th Avenue, Brooklyn, NY 11219, 1-800-278-4353, as agent under the Plan (the “Agent”). The Agent will open an account for each Shareholder under the Plan in the same name in which such Shareholder’s Shares are registered.

2. Whenever the Fund declares a capital gain distribution or an income dividend payable in Shares or cash, participating Shareholders will take the distribution or dividend entirely in Shares and the Agent will automatically receive the Shares, including fractions, for the Shareholder’s account in accordance with the following:

Whenever the Market Price (as defined in Section 3 below) per Share is equal to or exceeds the net asset value per Share at the time Shares are valued for the purpose of determining the number of Shares equivalent to the cash dividend or capital gain distribution (the “Valuation Date”), participants will be issued additional Shares equal to the amount of such dividend divided by the lower of the Fund’s net asset value per Share or the Fund’s Market Price per Share. Whenever the Market Price per Share is less than such net asset value on the Valuation Date, participants will be issued additional Shares equal to the amount of such dividend divided by the Market Price. The Valuation Date is the business day before the dividend or distribution payment date. If the Fund should declare a dividend or capital gain distribution payable only in cash, the Agent will, as purchasing agent for the participating Shareholders, buy Shares in the open market, or elsewhere, for such Shareholders’ accounts after the payment date, except that the Agent will endeavor to terminate purchases in the open market and cause the Fund to issue the remaining Shares if, following the commencement of the purchases, the Market Price of the Shares exceeds the net asset value. These remaining Shares will be issued by the Fund at a price equal to the lower of the Fund’s net asset value per Share or the Market Price.

In a case where the Agent has terminated open market purchases and caused the issuance of remaining Shares by the Fund, the number of Shares received by the participant in respect of the cash dividend or distribution will be based on the weighted average of prices paid for Shares purchased in the open market and the price at which the Fund issues remaining Shares. To the extent that the Agent is unable to terminate purchases in the open market before the Agent has completed its purchases, or remaining Shares cannot be issued by the Fund because the Fund declared a dividend or distribution payable only in cash, and the Market Price exceeds the net asset value of the Shares, the average Share purchase price paid by the Agent may exceed the net asset value of the Shares, resulting in the acquisition of fewer Shares than if the dividend or capital gain distribution had been paid in Shares issued by the Fund.

The Agent will apply all cash received as a dividend or capital gain distribution to purchase shares of common stock on the open market as soon as practicable after the payment date of the dividend or capital gain distribution, but in no event later than 45 days after that date, except when necessary to comply with applicable provisions of the federal securities laws.

3. For all purposes of the Plan: (a) the Market Price of the Shares on a particular date shall be the average of the volume weighted average sale prices or, if no sale occurred then the mean between the closing bid and asked quotations, for the Shares on each of the five trading days the Shares traded ex-dividend immediately prior to such date, and (b) net asset value per share on a particular date shall be as determined by or on behalf of the Fund.

4. The open market purchases provided for herein may be made on any securities exchange on which the Shares are traded, in the over-the-counter market, or in negotiated transactions, and may be on such terms as to price, delivery, and otherwise as the Agent shall determine. Funds held by the Agent uninvested will not bear interest, and it is understood that, in any event, the Agent shall have no liability in connection with any inability to purchase Shares within 45 days after the initial date of such purchase as herein provided, or with the timing of any purchases effected. The Agent shall have no responsibility as to the value of the Shares acquired for the Shareholder’s account.

Additional Information (Unaudited)

5. The Agent will hold Shares acquired pursuant to the Plan in noncertificated form in the Agent’s name or that of its nominee. At no additional cost, a Shareholder participating in the Plan may send to the Agent for deposit into its Plan account those certificate shares of the Fund in its possession. These Shares will be combined with those unissued full and fractional Shares acquired under the Plan and held by the Agent. Shortly thereafter, such Shareholder will receive a statement showing its combined holdings. The Agent will forward to the Shareholder any proxy solicitation material and will vote any Shares so held for the Shareholder only in accordance with the proxy returned by the Shareholder to the Fund.

6. The Agent will confirm to the Shareholder each acquisition for the Shareholder’s account as soon as practicable but not later than 60 days after the date thereof. Although the Shareholder may from time to time have an individual fractional interest (computed to three decimal places) in a Share, no certificates for fractional Shares will be issued. However, dividends and distributions on fractional Shares will be credited to Shareholders’ accounts. In the event of a termination of a Shareholder’s account under the Plan, the Agent will adjust for any such undivided fractional interest in cash at the opening market value of the Shares at the time of termination.

7. Any stock dividends or split Shares distributed by the Fund on Shares held by the Agent for the Shareholder will be credited to the Shareholder’s account. In the event that the Fund makes available to the Shareholder the right to purchase additional Shares or other securities, the Shares held for a Shareholder under the Plan will be added to other Shares held by the Shareholder in calculating the number of rights to be issued to such Shareholder. Transaction processing may either be curtailed or suspended until the completion of any stock dividend, stock split, or corporate action.

8. The Agent’s service fee for handling capital gain distributions or income dividends will be paid by the Fund. The Shareholder will be charged a pro rata share of brokerage commissions on all open market purchases.

9. The Shareholder may terminate the account under the Plan by notifying the Agent. A termination will be effective immediately if notice is received by the Agent three days prior to any dividend or distribution payment date. If the request is received less than three days prior to the payment date, then that dividend will be invested, and all subsequent dividends will be paid in cash.

10. These terms and conditions may be amended or supplemented by the Fund at any time or times but, except when necessary or appropriate to comply with applicable law or the rules or policies of the Securities and Exchange Commission or any other regulatory authority, only by mailing to the Shareholder appropriate written notice at least 30 days prior to the effective date thereof. The amendment or supplement shall be deemed to be accepted by the Shareholder unless, prior to the effective date thereof, the Agent receives written notice of the termination of such Shareholder’s account under the Plan. Any such amendment may include an appointment by the Fund of a successor agent in its place and stead under these terms and conditions, with full power and authority to perform all or any of the acts to be performed by the Agent. Upon any such appointment of an Agent for the purpose of receiving dividends and distributions, the Fund will be authorized to pay to such successor Agent all dividends and distributions payable on Shares held in the Shareholder’s name or under the Plan for retention or application by such successor Agent as provided in these terms and conditions.

11. In the case of Shareholders, such as banks, brokers, or nominees, which hold Shares for others who are the beneficial owners, the Agent will administer the Plan on the basis of the number of Shares certified from time to time by the Shareholders as representing the total amount registered in the Shareholder’s name and held for the account of beneficial owners who are to participate in the Plan.

Additional Information (Unaudited)

12. The Agent shall at all times act in good faith and agree to use its best efforts within reasonable limits to insure the accuracy of all services performed under this agreement and to comply with applicable law, but assumes no responsibility and shall not be liable for loss or damage due to errors unless the errors are caused by its negligence, bad faith, or willful misconduct or that of its employees.

13. Neither the Fund nor the Agent will be liable for any act performed in good faith or for any good faith omission to act, including without limitation, any claim of liability arising out of (i) failure to terminate a Shareholder’s account, sell shares, or purchase shares, (ii) the prices which shares are purchased or sold for the Shareholder’s account, and (iii) the time such purchases or sales are made, including price fluctuation in market value after such purchases or sales.

– END –

|

HISTORICAL DISTRIBUTION SUMMARY

|

|

| |

|

|

|

|

|

|

|

|

|

| |

|

Investment

|

|

|

Return of

|

|

|

|

|

|

|

|